|

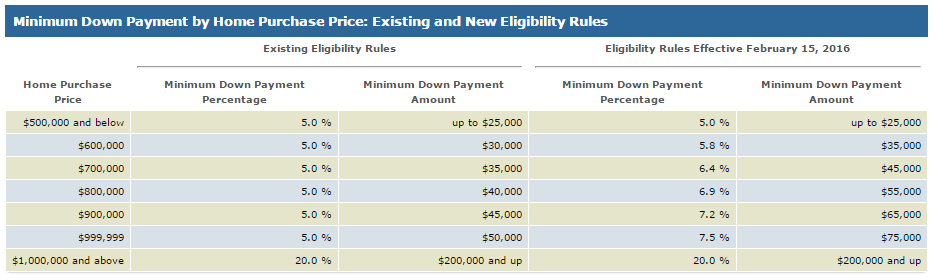

This past Friday Finance Minister Bill Morneau announced changes to down payment requirements. Effective February 15, 2016, the minimum down payment for new insured mortgages will increase from five per cent to 10 per cent for the portion of the house price above $500,000. The five per cent minimum down payment for properties up to $500,000 remains unchanged. Homes priced at more than $1 million by law require a minimum down payment of 20 per cent. Today's announcement therefore focuses on homes priced between $500,000 and $1 million. In the Mortgage Professionals Canada (MPC) Fall Report, Chief Economist, Will Dunning discusses why raising the down payment could cause problems for the housing market, including this cautionary observation: “Rising prices have made it increasingly difficult for first-time home buyers to accumulate down payments. Increasing down payment requirements would, most likely, severely dampen housing demands from people who are financially well-qualified to make their monthly mortgage payments.” MPC notes that the 10% requirement does represent a graduated approach while the Ministry of Finance commented that they believe this will only impact 1% of home purchasers, and this seems to play out when you really analyze the market. Prudent financial management of our housing and mortgage markets have so far prevented Canada from following the US and many other countries around the world into a real estate crisis that wiped out trillions of dollars in wealth for average citizens. It seems that this latest change is continuing that trend. Click here for the government’s official news release. Below is a handy chart showing what the min down payment would be for homes between $500K and $1MM  A closer look at these changes and some analysis of market demographics makes one realize that this latest change in mortgage rules does not have the “end of the world” implications that might be assumed. First, let’s eliminate the groups that this will have no impact on:

We know that the vast majority of homebuyers in the affected price range have at least 10% down and more frequently, 20% down (eliminating the need for high ratio insurance). Today’s first time buyers are more reliant than ever on “The Bank of Mom and Dad” particularly in the major cities with the highest prices. Even in situations where parents are not sitting on a big bank account, they often have houses that are fully paid, or have lots of equity which can be tapped into to help the children hit that magic 20% down payment – there are many benefits of this strategy – from the elimination of all high ratio insurance premiums to the availability of a 30 year amortization. Both of these examples will lower the monthly mortgage payments for the borrowers who are already probably stretching themselves a bit to get into the market.. The importance of a healthy and stable real estate market cannot be stressed enough as virtually every aspect of our economy is somehow linked to housing. If there is a higher level of confidence in the market, more investors will be looking at real estate as a safe and prudent place for their hard earned dollars and more homeowners and potential homeowners will have the confidence to buy their first, second, or third home without the fear of a correction wiping out their net worth. Here are some Frequently Asked Questions from the Government of Canada website What is this policy? This policy increases the minimum down payment from 5 per cent to 10 per cent on the portion of the house price above $500,000. This policy does not change the 5 per cent minimum down payment for properties up to $500,000. Why is the Government making this change at this time? The Government continuously monitors the housing market and is prepared to implement policy measures to maintain a healthy, competitive and stable housing market. The new measure reduces housing market risks by increasing borrower equity. This protects the stability of the housing market and the economy as a whole, as well as the interests of taxpayers who ultimately back government-guaranteed mortgage insurance. What will be the impact of the higher down payment requirement on the Canadian economy? Higher homeowner equity will help maintain a stable and secure housing market and balanced economic growth over the long-term. In the short term, this targeted measure will dampen somewhat the pace of housing activity over the next year, as some prospective homebuyers save for the increased minimum down payment. When does this measure take effect? The announced measure will take effect on February 15, 2016. I already have an insured mortgage. How will this change affect me? This measure applies only to new insured mortgage loans. Homeowners with an existing insured mortgage or those renewing existing insured mortgages will not be affected by this policy change as mortgage insurance is good for the life of any existing insured mortgage. I have already applied for mortgage insurance but my mortgage is not yet in place. How will this change affect me? The announced measure will take effect on February 15, 2016 and apply to new mortgage loan applications received on February 15, 2016 or later. Any mortgage insurance application received between December 11, 2015 and before February 15, 2016 that does not conform to the measures announced today must have a mortgage in place by July 1, 2016. How do higher minimum down payments for expensive properties relate to announcements made today by Canada Mortgage and Housing Corporation and the Office of the Superintendent of Financial Institutions? Canada Mortgage and Housing Corporation (CMHC) announced increases to guarantee fees charged to lenders for CMHC-sponsored securitization programs, National Housing Act Mortgage Backed Securities and Canada Mortgage Bonds. The Office of the Superintendent of Financial Institutions (OSFI) has also announced plans to consult on and update regulatory capital requirements for residential mortgages for federally regulated lenders and private mortgage insurers. Taken together, today’s actions will strengthen the resiliency of Canada’s housing finance system, reduce risks, and promote long-term stability and balanced economic growth. How will the measures announced today by the Government, CMHC and OSFI affect the cost and availability of mortgages to homebuyers? Combined, the measures are not expected to have a material impact on the level of mortgage rates, which remain at historically low levels, mortgage supply, or the competitive dynamics of the mortgage industry. What are the other four measures previously taken to contain risk in the housing market? Between 2008 and 2012, four rounds of changes were made to tighten eligibility rules for new insurable loans. These measures were aimed at encouraging insured borrowers to build and retain housing equity and take on debts they are able to service throughout the economic cycle. Among the significant changes were measures to: - Increase the minimum down payment to 5 per cent; - Decrease the maximum amortization period to 25 years; - Limit the maximum insurable house price to below $1 million; - Apply maximum debt service-to-income ratios; and, - Apply a mortgage rate stress test for mortgages with terms of less than 5 years or variable rates. More information on these measures can be found on the Department of Finance Canada website. If you have any questions about these changes and what they might mean to you, please contact me anytime. As an independent and experienced mortgage broker, I can look at the entire situation, ask the relevant questions, and provide the best options to help today’s homebuyers take advantage of what is best for their situation. I do not sell one lender’s product, and I'm not restricted by the rules of any one lender. Mortgage Brokers provide choice and multiple options with unbiased advice in today’s very complicated world of mortgages.

0 Comments

Leave a Reply. |

Hey There!Please Feel Free to Leave a Comment on my Blog Post! Categories

All

Archives

February 2019

Categories

All

|

- Home

- Apply Now

- Blog

-

Solutions

- Mortgage Pre-Approval

- First Time Home Buyers

- Repeat Buyers

- Mortgage Renewal/Switch

- Mortgage Refinance

- Mortgages For Self-Employed

- New Immigrant Mortgages

- Mortgages with Renovations

- Mortgages For Rental Properties

- Borrowed Down Mortgages

- Divorce and Your Mortgage

- Equity Mortgage Loans

- Private/Second Mortgages

- Credit Issues

- Useful Tools

- About

- Contact

- Home

- Apply Now

- Blog

-

Solutions

- Mortgage Pre-Approval

- First Time Home Buyers

- Repeat Buyers

- Mortgage Renewal/Switch

- Mortgage Refinance

- Mortgages For Self-Employed

- New Immigrant Mortgages

- Mortgages with Renovations

- Mortgages For Rental Properties

- Borrowed Down Mortgages

- Divorce and Your Mortgage

- Equity Mortgage Loans

- Private/Second Mortgages

- Credit Issues

- Useful Tools

- About

- Contact

RSS Feed

RSS Feed